Brookfield’s growth (referring to the combined Brookfield Corporation (BN) and Brookfield Asset Management (BAM) entities post-2022 restructuring) has been impressive from the 2020 lows through early 2026, particularly in fee-bearing capital and overall business scale. The original post’s claim (below) of a ~4x+ increase in combined market caps (from ~$45B in 2020 lows to ~$194B) aligns directionally with strong performance, though exact figures vary by timing and includes restructuring effects (BAM was spun out as the pure asset management play in 2022, while BN retained the operating businesses).

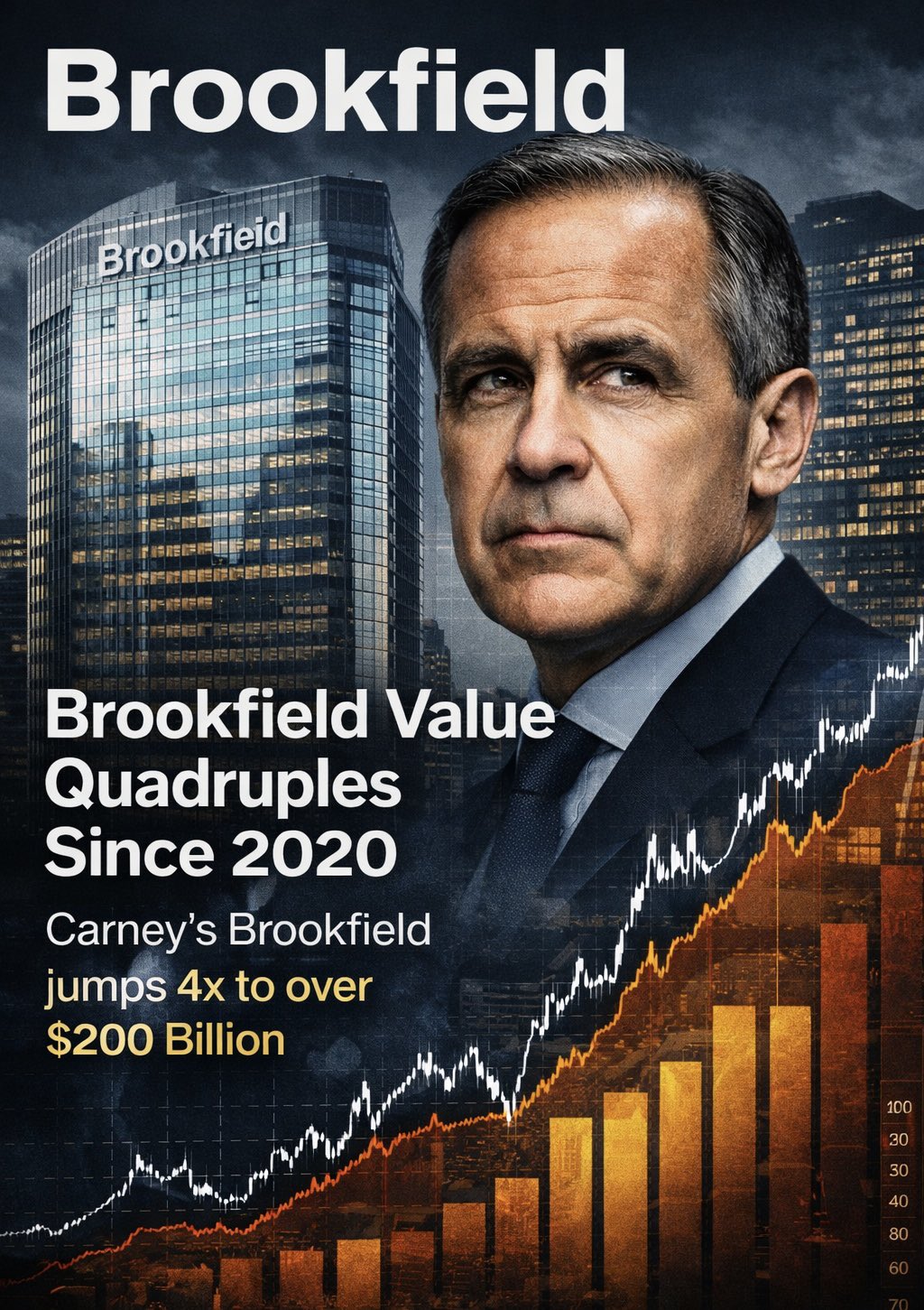

🚨Brookfield value quadrupled since 2020.

— wealthmoose (@wealthmoose) January 9, 2026

~$40–50B at the 2020 lows.

$200B+ today.

That’s a 4–5× jump in a few years.

Canada?🇨🇦

Running a $78B deficit this year.

Private capital is compounding.

Public finances are decaying.

Tell me again how this is “good management.”… pic.twitter.com/0WFSfyY1gb

Brookfield doubled its fee-bearing capital from ~$277B in 2020 to ~$580B by late 2025, with fee-related earnings roughly doubling as well. This reflects successful execution in alternative assets, especially infrastructure, renewables, and real assets—areas that have benefited from long-term trends like energy transition.

Comparison to Key Peers

Brookfield stands out among major alternative asset managers (Blackstone (BX), KKR, Apollo Global Management (APO)) for its heavy focus on real assets (infrastructure, renewables, real estate), which has provided more stability in certain market cycles compared to peers more concentrated in private equity or credit.

- Market Cap Snapshot (late 2025 / early 2026 estimates):

- Brookfield Corporation (BN): ~$104–111B USD (with some reports in CAD equivalent higher).

- Brookfield Asset Management (BAM): ~$88B (trading around $54/share).

- Combined Brookfield ecosystem: Well over $190B, supporting the post’s scale narrative.

- Blackstone (BX): Largest in the sector, often ~$150B+ (though with stock pullbacks from 2025 highs).

- KKR: ~$100B+ range, strong growth.

- Apollo: Significant scale (~$600–750B+ AUM targets), but market cap varies.

- Performance Since 2020:

- Brookfield delivered robust long-term growth, with BN showing ~119% total return over 5 years (roughly 2020–2025 period), though recent periods (e.g., TTM or YTD in 2025–2026) have been more modest (15–22%).

- BAM (the pure management vehicle) has lower volatility but more moderate returns in recent years (~44% over 5 years, with YTD/TM modest in 2025–2026).

- Peers like Blackstone and KKR often showed stronger short-term runs in certain years (e.g., post-2020 recovery in private equity), but faced more volatility in 2025 (e.g., BX, KKR, and APO stocks down 29–31% from 2025 highs amid market rotations and private equity headwinds).

- Brookfield’s real asset tilt has helped it weather some cycles better, with less dramatic drawdowns compared to more PE-heavy peers.

- Other Metrics:

- Valuation: BAM trades at a higher P/E (38x) than the peer average (37x), seen as “expensive” relative to some comparables.

- Growth Outlook: Analysts project strong earnings/revenue growth for BAM (e.g., 50%+ revenue CAGR in forecasts), outpacing broader markets.

- Dividend Yield: BAM offers ~3.3%, competitive with peers like Blackstone.

Overall, Brookfield’s growth has been among the strongest in the alternative asset space since 2020, especially when viewed through the lens of fee-bearing capital expansion and real asset focus. It hasn’t always outpaced every peer in short-term stock returns (e.g., Blackstone or KKR had explosive periods), but its diversified, long-duration approach has delivered consistent compounding with relatively lower volatility in some environments. This has made it a standout for investors seeking exposure to infrastructure and transition themes. Peers remain formidable, with Blackstone holding the top spot by scale in many metrics.

Leave a Reply

You must be logged in to post a comment.